Finance Departments Need More Advanced Analytics

Analytics is nothing new in finance. Chief financial officers (CFOs) and their staffs have been using them for years to crunch numbers and draw insight from balance sheets, income statements and cash-flow statements. But how analytics is being deployed appears to be shifting.

“Finance departments are demanding more self-service analytics, more use of advanced analytics, and easier access to finance and operational data in order to analyze it,” said Robert Kugel, senior vice president and research director at Ventana Research. “Advances in the tools for analyzing and reporting the data have made it possible to assess financial performance, process quality, operational status, risk and even governance and compliance in every aspect of a business.”

One hurdle in the finance department's adoption of more robust analytics has been an over-reliance on spreadsheets. Long the staple of finance, Ventana Research found that the limited analytical capabilities of spreadsheets make it tough for finance executives to get the most out of their data.

“Reliance on spreadsheets makes it difficult to produce accurate and timely analytics,” Kugler said.

Most CFOs are good at the basics: financial statement analyses, modeling, forecasting and planning. Only a relative handful, however, apply economic and market indicators, price optimization techniques or profitability analysis on a regular basis. The result is that the bulk of finance departments are not harnessing predictive analytics in planning and forecasting.

Beyond Spreadsheet Automation

John Van Decker, an analyst at Gartner, concurs with the view that spreadsheet-centric analytics have been holding back finance.

“Analytics has always been a strong component of finance departments such as dashboards, visualization technologies, budget planning and forecasting,” he said. “But now they are beginning to look beyond spreadsheets for a central location for the budget system, Excel is becoming more of a collector than a central financial database.”

This is leading those CFOs on the vanguard to utilize analytics for more strategic and predictive capabilities within finance. Van Decker recommended that CFOs stop looking at analytics as a purely software evaluation exercise. Instead, he encouraged them to pay as much attention to their business processes as part of a finance transformation project.

“Automating your spreadsheets is not enough,” he said. “Done correctly, the combination of analytics with better business processes can lead to better and faster decision making.”

Kugel highlighted one area of attack on business processes, noting that the freshness of data must be improved for analytics to be truly useful. On that score, Ventana Research found that less than half of finance departments are able to deliver key metrics and performance indicators within a week of a period’s end. This, he said, is often too slow to respond to opportunities or threat.

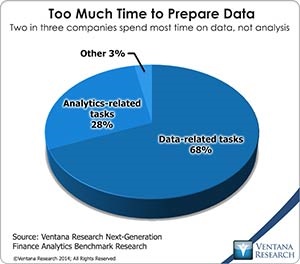

The reason behind this is that those doing the analyses get bogged down on data-related tasks. This leaves them only a quarter of available time for actual analysis. Data accuracy, timeliness, relevance and consistency have a major impact on analysis quality, Kugel said.

Van Decker also suggested that finance departments step out of their comfort zone of relying on a mega-suite of software to meet their every need. Increasingly, finance is allowed to choose its own solutions. Freed from the constraints of IT-centric purchasing of software, best of breed is now driving a lot of purchasing.

“The big mega-suite in the sky is no longer the ideal,” Van Decker said.

Strategic Analysis, not Transactions

In addition to their usual seat at the executive table in assisting with the development of strategy, it often falls to the CFO to be the primary enterprise monitor of business alignment with strategy and also with strategy execution. To be effective in this role, the CFO has to become skilled in developing and reporting metrics related to strategy execution.

Too often an organization has hundreds of metrics available on its dashboards and management reporting packages, when a reasonable number to focus on would be in the 20-25 range. This can bring about situations where they end up measuring the same thing in multiple different ways, when they would be better served in identifying the best metrics for the desired objective.

“Analytics comes into play in determining correlation, causation and relevance, and in identifying those best metrics,” said Leo Sadovy, marketing manager at SAS.

For decades, he added, the discussion in the financial planning and analysis (FP&A) community has been around how to move from being primarily transaction oriented into being a valued business partner with a key role in transforming the organization. The reality has been an 80/20 transaction/transformation ratio, while the goal has been to reverse it and achieve 80/20 transformation/ transaction. The industry is at perhaps the 50/50 point today, Sadovy estimated with some firms further along than others.

“To get to 80 percent valued partner activities means becoming much more efficient at the transactional aspects, which is where analytics and business intelligence come into play,” he said.

Analytics and KPIs

According to SAS, the biggest single area where analytics can cut down on transactional activities is analytical or driver-based forecasting. The idea is to stop forecasting individual line items directly, but instead to focus on forecasting key business drivers. If you can nail down the key half-dozen drivers of a business and get a handle on the other 15 or so that have a lesser but noticeable impact, you can stop trying to forecast 20-30 line-items-per-cost-center times hundreds or thousands of costs centers, and concentrate on addressing the key drivers.

“Once your staff starts talking the language of drivers rather than profit-and-loss line items, they put themselves in a position to work with line business management in a value-add, decision support manner,” said Sadovy.

SAS has noticed steady adoption by finance teams of cost and profitability management tools, also known as activity-based costing management. Sadovy challenged those not using this technology to shrug off their industrial accounting legacy, and use these tools to properly understand true costs and profitability by product and customer. Instead, he said, we are stuck using accounting techniques appropriate when overhead allocations were 25 percent or less of a business’ costs. Today it is typical to see 45 percent margins in high tech, and in many service industries like banking or telecom there is little or no direct material and cost anyhow.

“If you are allocating overhead and indirect costs to products and customers based on nothing more sophisticated than a broad-brush, high-level, total revenue or total cost basis, you probably do not have an accurate picture of the true cost and profitability of either,” he said.

Another specific application of analytics to finance has arisen in the banking and capital markets, where the stress testing and regulatory capital requirements emerging from legislation such as Dodd-Frank require close collaboration between the CFO, the CRO (chief risk officer) and the head of investments. Restructuring of the asset portfolio has balance sheet, cash and regulatory capital requirement implications every time it’s done, whether that’s part of a deliberate monthly or quarterly plan, or overnight in response to market changes the previous day. Using analytics behind integrated capital planning and management helps meet economic and regulatory targets, align strategies, ensure consistency, transparency and auditability, and integrate funding strategy into capital reporting, Sadovy said.

“The way to become more analytical in finance and add more value to the business is to get off your reliance on spreadsheets,” Sadovy said. “If you are still relying on spreadsheets, you never get to go home early on Fridays.”

Drew Robb is a freelance writer specializing in technology and engineering. Currently living in Florida, he is originally from Scotland, where he received a degree in geology and geography from the University of Strathclyde. He is the author of Server Disk Management in a Windows Environment (CRC Press).

Drew Robb is a writer who has been writing about IT, engineering, and other topics. Originating from Scotland, he currently resides in Florida. Highly skilled in rapid prototyping innovative and reliable systems. He has been an editor and professional writer full-time for more than 20 years. He works as a freelancer at Enterprise Apps Today, CIO Insight and other IT publications. He is also an editor-in chief of an international engineering journal. He enjoys solving data problems and learning abstractions that will allow for better infrastructure.