Data Center Accelerator Market to Hit USD 168 Bn by 2032

Page Contents

Market Overview

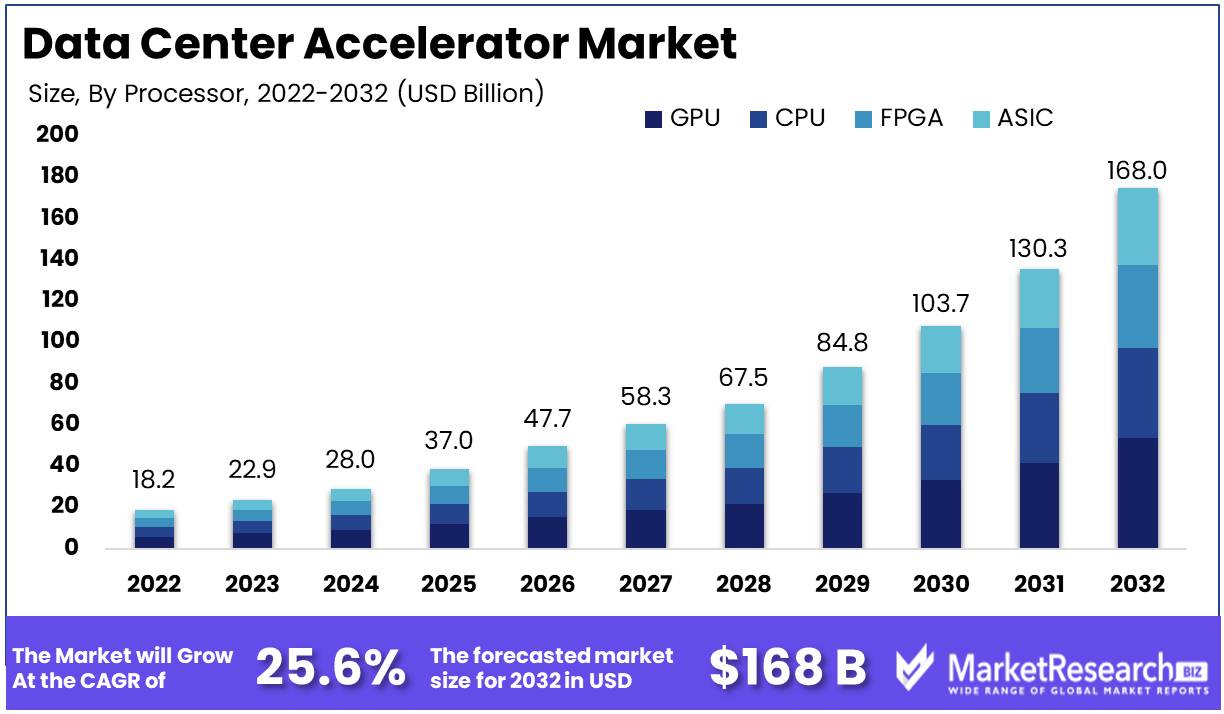

Published Via 11Press : Data Center Accelerator Market size is expected to be worth around USD 168 Bn by 2032 from USD 18.2 Bn in 2022, growing at a CAGR of 25.6% during the forecast period from 2022 to 2032.

Data center accelerator market growth has experienced rapid expansion over the last several years due to rising demand for high-performance computing and data-intensive applications. Data centers play an essential role in modern technological ecosystems by providing the infrastructure necessary for storing, processing, and managing massive amounts of information. To optimize efficiency and performance in their centers, organizations are turning towards data center accelerators as an aid.

Data center accelerators are specialized hardware or software components designed to streamline data center operations. By offloading tasks like data compression, encryption, and decompression from traditional CPUs to accelerators, data centers can achieve higher performance, lower power consumption, and greater cost efficiency.

There are various data center accelerators on the market, such as graphics processing units (GPUs), field-programmable gate arrays (FPGAs), application-specific integrated circuits (ASICs), and neural processing units (NPUs). GPUs were initially designed for gaming and graphics rendering but have become popular choices for data centers thanks to their parallel processing abilities. FPGAs provide greater flexibility and reconfigurability, making them suitable for a wider array of applications. ASICs, on the other hand, are custom-built for specific tasks and offer high performance and energy efficiency. NPUs were specifically created to accelerate artificial intelligence and machine learning workloads that have become increasingly important within data centers.

The data center accelerator market has seen widespread adoption across industries such as IT/telecommunications, healthcare, manufacturing, finance and automotive. Due to advances in artificial intelligence, big data analytics and the Internet of Things (IoT), data center accelerator demand is expected to only increase further.

Key players in the data center accelerator market include leading semiconductor companies like NVIDIA, Intel, Xilinx and AMD. These firms continually innovate and release new products designed to meet the ever-evolving needs of data centers. Furthermore, several start-ups are entering with specialty accelerators designed for specific applications or workloads.

Request Sample Copy of Data Center Accelerator Market Report at: https://marketresearch.biz/report/data-center-accelerator-market/request-sample

Key Takeaways

- Due to an increased demand for high-performance computing and data intensive applications, the data center accelerator market is experiencing unprecedented expansion.

- Data center accelerators offload processing tasks from CPUs, enhancing performance, power efficiency and cost effectiveness.

- Data center accelerators include GPUs, FPGAs, ASICs and NPUs – each offering their own advantages and applications.

- Data center accelerators have found use across industries, from IT and healthcare to manufacturing, finance, and automotive.

- Market leaders such as NVIDIA, Intel, Xilinx and AMD lead in innovation and product release.

- Start-ups have also entered the market, offering customized accelerators tailored specifically for certain workloads or applications.

- AI, big data analytics and IoT technologies are driving up demand for data center accelerators.

- Future prospects of data center accelerator markets look bright as data centers continue to advance and scale, necessitating further improvements in performance and energy efficiency.

Regional Snapshot

- North America and especially the United States lead the data center accelerator market due to their advanced technological infrastructure and presence of major technology giants. North America boasts a high concentration of data centers that have led to technological innovations like artificial intelligence (AI), machine learning (ML), and big data analytics; therefore data center accelerators are in high demand here as processing large amounts of data supports advanced applications in industries like finance, healthcare and e-commerce.

- Europe is seeing significant expansion in the data center accelerator market as businesses adopt digital transformation strategies across the region. Countries like Germany, UK and France lead in terms of infrastructure investments and accelerator deployment; additionally this market benefits from strict data privacy regulations encouraging organizations to build robust data centers equipped with accelerators to ensure efficient processing.

- Asia Pacific region data center accelerator market is experiencing explosive growth driven by rising adoption of cloud computing, AI and IoT technologies. China, Japan and India have invested significantly in data center infrastructure to support their respective digital transformation initiatives. Furthermore, growing populations, expanding internet penetration rates, mobile device proliferation and increased data traffic have created an increasing need for data center accelerators to manage rising data traffic loads.

- Latin America is an emerging market for data center accelerators with rising investments in infrastructure. Brazil, Mexico and Argentina have all played an essential role in contributing to Latin American's market expansion; adoption of cloud services, e-commerce expansion and data analytics driving demand for accelerators; governments are also undertaking initiatives to enhance connectivity and digital infrastructure which further support its expansion.

- Middle East and Africa organizations are seeing an increase in adoption of data center accelerators as they utilize advanced technologies for economic diversification and digital transformation. Nations like United Arab Emirates, Saudi Arabia and South Africa are investing heavily in data centers infrastructure in support of fintech, e-commerce and healthcare businesses that require large data sets for processing or analysis; fueling demand for accelerators.

For any inquiries, Speak to our expert at: https://marketresearch.biz/report/data-center-accelerator-market/#inquiry

Drivers

Demand for High-Performance Computing Systems

High-performance computing (HPC) applications like AI, machine learning and big data analytics is a significant driver of data center accelerator market growth. Accelerators increase performance of these compute-intensive tasks by offloading processing from CPUs allowing faster and more efficient data processing.

Data-Intensive Workloads

The exponential expansion of data-intensive workloads across industries such as healthcare, finance and manufacturing is driving demand for data center accelerators that can handle large volumes of data quickly and enable real-time analytics and decision-making capabilities. These accelerators support real-time analytics while supporting real-time decision making processes.

AI Advancements

Artificial Intelligence (AI), including deep learning and neural networks, are driving data center accelerator adoption. AI applications require ample computational power that GPUs and NPUs provide. As a result, organizations can train and deploy complex AI models more quickly.

Energy Efficiency and Cost Optimization.

Data center operators are increasingly focused on energy efficiency and cost optimization in their operations. Accelerators offer improved energy efficiency by offloading processing from CPUs, which reduces power consumption. In addition, accelerators deliver greater performance at reduced costs; making them an appealing solution for organizations looking to streamline their data center operations.

Restraints

High Initial Investment Costs

Implementation of data center accelerators requires significant upfront expenses, including purchasing of hardware and software components that must be integrated with existing infrastructure. This initial investment may prove prohibitive to organizations with tight budgets attempting to integrate accelerators.

Compatibility and Integration Issues

Integration of data center accelerators can present many difficulties when dealing with legacy systems or heterogeneous environments, namely compatibility issues, software optimization and seamless integration; all tasks which may take additional time and resources.

Limited Standardization

The data center accelerator market lacks standard programming models and interfaces, making it challenging for developers and system integrators to effectively use accelerators. A lack of widely adopted standards may inhibit interoperability, portability and software development efforts resulting in slower adoption rates and greater implementation complexities.

Cooling Requirements and Energy Usage Restrictions

Data center accelerators are power-hungry components that produce considerable heat. Their increased consumption and dissipation requirements can strain existing cooling infrastructure and increase operational costs, so data centers must address them by installing efficient cooling systems and optimizing power management strategies to ensure they make optimal use of accelerators.

Opportunities

Hardware Development in AI

As AI advances continue to create dedicated chips and architectures, data center accelerator markets could see significant advantages. Advancements made with GPU, NPU, FPGA technologies as well as dedicated AI accelerators will increase performance while opening up new avenues of accelerated computing.

Edge computing

which data processing occurs at its source – presents data center accelerators with unique opportunities. Edge devices may use accelerators for real-time analytics, AI inference and video processing tasks; with demand for low latency solutions driving acceleration's adoption in edge environments.

Hybrid and Multi-Cloud Environments

As more organizations shift to hybrid and multi-cloud architectures, data center accelerators stand to reap great rewards. Accelerators provide organizations with a way to optimize workloads across distributed cloud environments for increased performance and reduced latency – with multi-cloud strategies becoming more widely adopted, demand will only increase for accelerators capable of seamless workload distribution.

Quantum Computing

This holds great promise for data center accelerators. Quantum accelerators can maximize quantum computing capabilities for faster and more complex computations while opening up new market opportunities. As this field matures further, data centers will need specialized accelerators in order to fully take advantage of its full potential and realize all its advantages.

Take a look at the PDF sample of this report: https://marketresearch.biz/report/data-center-accelerator-market/request-sample

Challenges

Cooling and Power Consumption

Data center accelerators produce significant heat and have higher power requirements compared to traditional CPUs, making managing heat dissipation and cooling mechanisms challenging – leading to increased energy consumption and operational costs as a result. Overcoming such challenges and optimizing energy efficiency are essential to ensure sustainable data centers.

Interoperability and Standardization

Data center accelerator market comprises an assortment of hardware and software solutions with different architectures and programming models. Interoperability issues and lack of standardization may impede portability between platforms and vendors; creating industry-wide standards could foster compatibility while alleviating integration challenges.

Security and Data

Accelerated computing introduces additional security challenges. Accelerators must protect data processed by them from vulnerabilities such as side-channel attacks or compromised firmware, to prevent vulnerabilities such as side-channel attacks. Ensuring the security and integrity of workloads processed by accelerators as well as implementing robust data protection measures are primary tasks of data center operators.

Technology Landscape in Transition

Data center accelerator markets are rapidly developing, and keeping up with hardware and software innovations can be challenging. Data center operators must remain abreast of technological changes and adapt their infrastructure accordingly in order to remain competitive.

Market Segmentation

By Processor

- GPU

- CPU

- FPGA

- ASIC

By Type

- Cloud Data Center

- HPC Data Center

By Application

- Deep Learning Training

- Public Cloud Interface

- Enterprise Interface

Key Players

- Dell Technologies Inc.

- International Business Machines Corp.

- Intel Corporation

- Cisco Systems Inc.

- Lenovo Group Ltd.

- Hewlett Packard Enterprise Development LP

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- XILINX Inc.

- Achronix Semiconductor Corporation

Report Scope

| Report Attribute | Details |

| Market size value in 2022 | USD 18.2 Bn |

| Revenue Forecast by 2032 | USD 168 Bn |

| Growth Rate | CAGR Of 25.6% |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and Rest of the World |

| Historical Years | 2017-2022 |

| Base Year | 2022 |

| Estimated Year | 2023 |

| Short-Term Projection Year | 2028 |

| Long-Term Projected Year | 2032 |

Recent Developments

- In April 2023, NVIDIA announced that they had successfully shipped their 100 Millionth GPU. NVIDIA GPUs are widely used by data center managers for various applications such as artificial intelligence, machine learning and graphics processing.

- In May 2023, Intel announced the introduction of their Xeon Scalable processors with integrated AI acceleration technology for use by data centers to increase performance for AI workloads.

- In June 2023, AMD announced the introduction of its Instinct MI200 accelerator series for data centers to accelerate AI, machine learning and high-performance computing workloads. These accelerators aim to help data centers accelerate an array of workloads such as AI, machine learning and high-performance computing.

FAQ

1. What is a Data Center Accelerator?

A. Data center accelerators are specially-made hardware or software components intended to increase the performance and energy efficiency of data centers. By offloading specific processing tasks like data compression, encryption or artificial intelligence workloads from the CPU, such as compression/encryption/AI workloads from being performed within datacenters themselves resulting in improved speed and energy efficiency.

2. What types of data center accelerators exist?

A. There are various types of data center accelerators, including GPUs, FPGAs, ASICs and neural processing units (NPUs). Each has its own distinct architecture and properties that suit particular workloads.

3. What are the drivers behind data center accelerator adoption?

A. Data center accelerators have seen increasing adoption due to factors like increased demand for high-performance computing, the proliferation of artificial intelligence/machine learning applications, the need for efficient big data analytics solutions and the proliferation of cloud computing/virtualization technologies.

4. What are the primary challenges associated with data center accelerators?

A. Data center accelerators present several unique challenges, including high initial investment costs and integration challenges with existing infrastructure, limited scalability in certain environments, and requiring specific skills and knowledge for effective usage and management of accelerators.

5. How can data center accelerators contribute to greater energy efficiency?

A. Data center accelerators can play a pivotal role in energy efficiency by offloading compute-intensive tasks from general-purpose CPUs onto dedicated accelerators that may be more energy efficient for specific workloads. This reduces overall power consumption across infrastructure as accelerators tend to be more energy efficient than general-purpose CPUs when handling compute-intensive processes.

6. Are data center accelerators compatible with existing software and infrastructure?

A. Data center accelerators may require specific libraries, drivers or APIs in order to remain compatible with existing software and infrastructure. While compatibility issues may arise from time to time, most accelerators are designed with compatibility in mind so as to integrate seamlessly with popular operating systems, programming languages and frameworks for easy system integration.

7. How can data center accelerators support AI and machine learning applications?

A. Data center accelerators such as GPUs and NPUs are specially tailored to handle the computational demands associated with artificial intelligence and machine learning applications. They excel in performing parallel computations, optimizing matrix operations, supporting deep learning algorithms, and expediting training and inference processes in AI workloads thereby speeding up training and inference processes for AI workloads.

Contact us

Contact Person: Mr. Lawrence John

Marketresearch.Biz

Tel: +1 (347) 796-4335

Send Email: [email protected]

Content has been published via 11press. for more details please contact at [email protected]

The team behind market.us, marketresearch.biz, market.biz and more. Our purpose is to keep our customers ahead of the game with regard to the markets. They may fluctuate up or down, but we will help you to stay ahead of the curve in these market fluctuations. Our consistent growth and ability to deliver in-depth analyses and market insight has engaged genuine market players. They have faith in us to offer the data and information they require to make balanced and decisive marketing decisions.